Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

Is it worth the wait for the best interest rate?

Interest rates are still in the headlines. A friend tells you they got a better rate than you. The news announces rates moved up or down. Buyers spend hours refreshing mortgage apps and waiting for the “perfect” moment to lock.

But how much does a small rate change actually matter?

Sometimes an eighth of a percent is barely noticeable. Other times, it can completely change a buyer’s ability to purchase a home. Let’s put some real numbers behind it

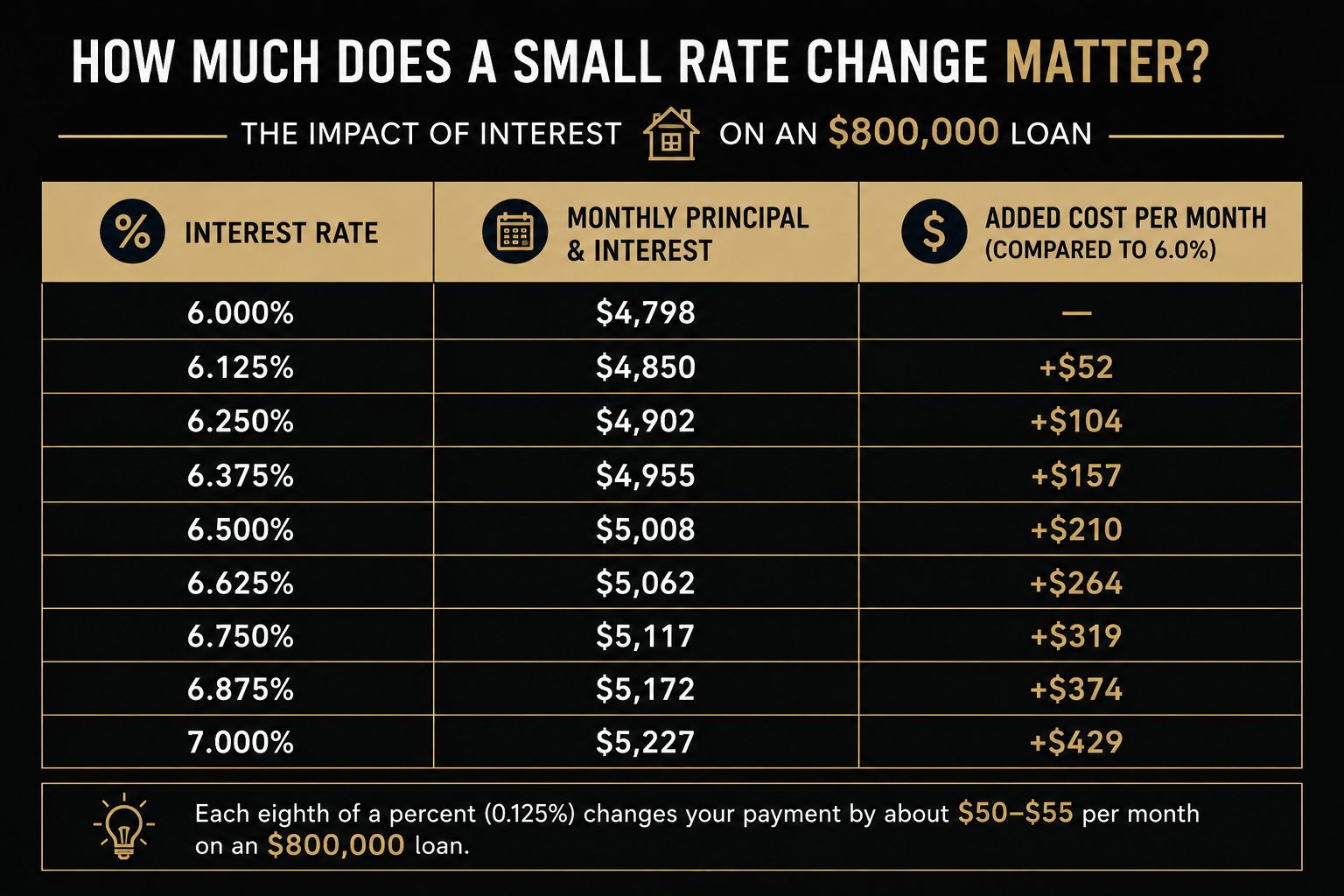

Using an $800,000 loan amount with a 30-year fixed mortgage (principal and interest only), here is how small changes in interest rates affect the monthly payment:

When buyers see this chart, many have the same reaction: “Wait, that’s it?”

And honestly, for many buyers, that’s a fair response. A difference of roughly $50 per month for each eighth of a percent may not significantly change your day-to-day life if you are comfortably qualified and purchasing a home that fits well within your budget.

But that same $50 can mean something entirely different for another buyer.

When an Eighth of a Percent Doesn’t Matter Much

Sometimes buyers become so focused on chasing the absolute lowest interest rate that they lose sight of the bigger picture. If you find a home that checks all of your boxes, fits your lifestyle, and the payment is comfortable, waiting months for rates to improve may not be the best financial decision.

A slightly higher interest rate may cost you an extra dinner out each month, but what happens while you wait?

The home you love may sell to someone else. Prices in your desired neighborhood may increase. Your rent payments continue without building equity.

Interest rates are only one piece of the homeownership puzzle.

The Hidden Cost of Waiting for the “Perfect” Rate

Many buyers tell me they are waiting until rates drop before they begin their home search. It’s completely understand, a lower interest rate makes homeownership more affordable. The challenge is that no one can accurately predict when, or if, that drop will happen.

While you are waiting the right home may come on the market and sell to another buyer. Home values may continue to appreciate. Your rent may increase. Interest rates may actually move higher instead of lower. You won’t be building equity.

Trying to perfectly time interest rates is a little like trying to perfectly time the stock market. It sounds simple, but very few people can do it consistently.

The better question isn’t: “How do I get the absolute lowest interest rate?”

It is: “Does this home fit my life, and does the monthly payment fit comfortably within my budget today?”

When an Eighth of a Percent Matters A Lot

Now let’s look at the other side. For some buyers, an eighth or a quarter of a percent can be the difference between moving forward and having to step back entirely.

Mortgage lenders use debt-to-income ratios (DTI) to determine how much monthly debt a buyer can comfortably support. A small increase in your projected housing payment can sometimes push a buyer over the qualification limit.

This becomes especially important when:

- You are shopping at the top of your budget.

- You have a higher debt-to-income ratio.

- Property taxes or homeowners insurance come in higher than expected.

- Interest rates rise before your loan is locked.

I have heard stories of buyers who were fully approved at the beginning of their home search, but because rates moved before they locked, they no longer qualified for the same home price, or even the home they had under contract. For these buyers, an eighth of a percent isn’t just a number. It can change the entire outcome.

Why Rate Locks Matter

One of the most important conversations you can have with your lender is about rate lock strategy. A rate lock protects you from market movement while your loan is being processed. It provides certainty in a process where many things can change.

Could rates drop after you lock? Absolutely. Could they rise? Absolutely.

That is why it is important to work with a lender who can walk you through your options, including whether they offer a rate renegotiation or “float-down” policy if rates drop significantly during your lock period.

The Bigger Lesson

Interest rates matter. But so does context.

A buyer who is comfortably qualified should not panic over every eighth of a percent. A buyer who is near their qualification limit needs to pay very close attention.

The goal should never be to find the lowest interest rate at any cost. The goal is to find a home that works for your life and a payment that allows you to sleep well at night. Because sometimes an eighth of a percent is just fifty dollars, and sometimes it’s the difference between getting the keys and missing out.

The great part is you don’t have to navigate this alone. Whether you’re ready to lock in a rate today or just want to figure out exactly how much purchasing power you have in today’s market I would be thrilled to help you navigate this journey. Reach out and we can figure out your next steps.